Tuesday, 13th April 2021

The New Tax Year has started, 6th April 2021 just in case you missed it! Which means there are a whole host of new rates, allowances and reliefs. So what’s new for the 2021/2022 tax year?

How do these affect you, both business owners and individuals?

The Highlights

- Personal Tax, National Insurance and allowances

- Apprenticeships and Minimum Wage changes

- DLA, Company Cars, Vans and Fuel Benefit

- Student Loans and Postgraduate Loans

- Other personal tax reliefs and allowances

- Entrepreneurs Relief changes

- VAT, Corporation Tax, workplace pensions and allowances

- Other Taxes and COVID-19 Support

Read on to find out more and how we at Onyx can help you make the most out of this year’s changes.

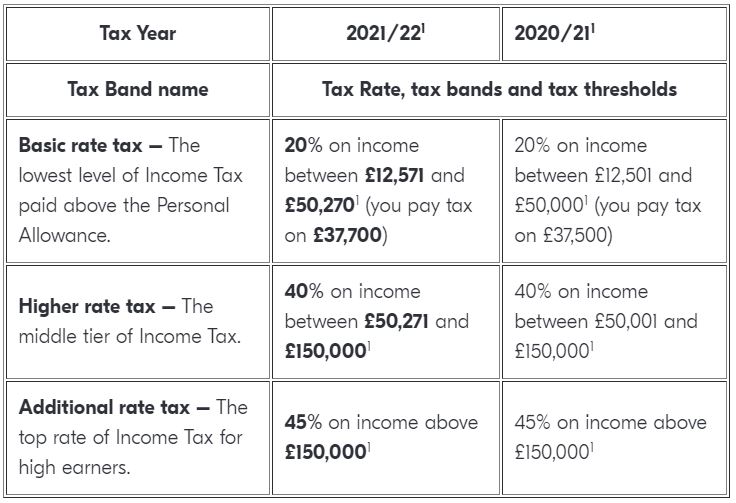

1 – Personal Tax, thresholds and allowances

The Personal Allowance and threshold for paying the Higher Rate of income tax have slightly increased.

The Personal Allowance has increased to £12,570 (2020/21 £12,500). The threshold for paying the Higher Rate of income tax (which is 40%) has increased to £50,270 (2020/21 £50,000). These will remain frozen until 2026.

The Personal Allowance is reduced by £1 for every £2 earned over £100,000.

A table of the income tax rates for England and Wales is below. The rates are slightly different if you are a Scottish taxpayer1. If this is you, then contact us now to find out how your tax bill will be calculated.

Are you a director and shareholder of your own company?

To maximise your tax efficiency as a company Director and Shareholder in the 2021/22 tax year, we recommend a director salary of £8,840 and dividends of up to £41,430.

Contact Onyx now to find out how we can ensure you maximise on the tax efficiency of salary and dividends for this tax year.

Find out now if you could be at risk of being a higher rate taxpayer. The steps needed to be taken to minimise the shock of a higher than expected tax bill. Also how to manage the cashflow.

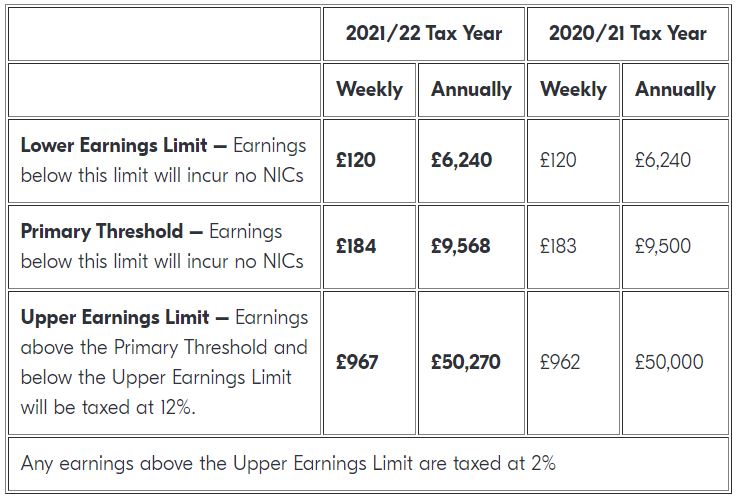

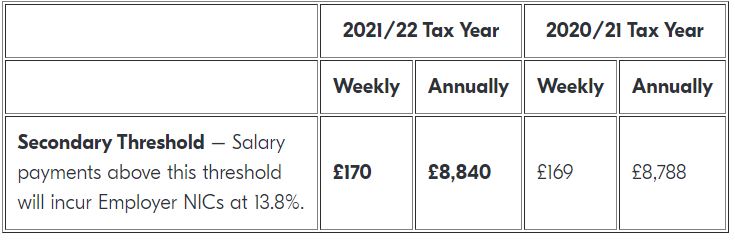

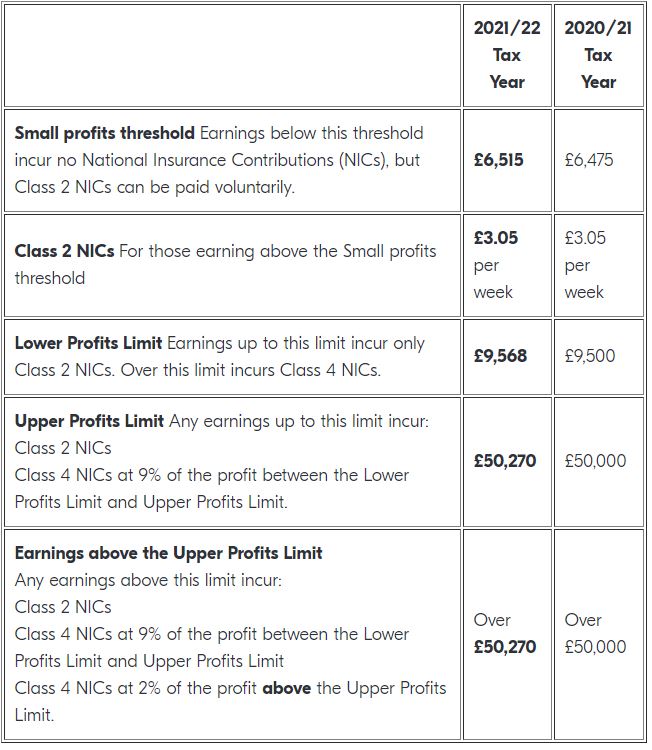

National Insurance

There are small increases to each of the income thresholds for both employee and employer national insurance contributions and for self-employed earnings.

– Employee National Insurance Contributions

– Employer National Insurance Contributions

As an employer, you may be eligible to claim Employment Allowance to reduce your Employer’s National Insurance bill.

– Self Employed National Insurance Contributions

Need help with your payroll calculations and want to ensure the correct amount of contributions are paid over? Perhaps you are not sure how much you will pay on your self-employed earnings. Contact Onyx now and we will explain how these new rates will be applied.

Dividend Allowance

There is no change to the tax-free dividend allowance and the dividend tax rates in the 2021/22 tax year remain as follows:

- The tax-free dividend allowance is £2,000

- Basic-rate taxpayers pay 7.5% on dividends

- Higher-rate taxpayers pay 32.5% on dividends

- Additional-rate taxpayers pay 38.1% on dividends.

2 – Apprenticeships, National Minimum Wage and National Living Wage

– Apprenticeships

The apprentice hiring incentive in England was extended to September 2021 and the payment increased to £3,000. A flexi-apprenticeship scheme was also announced that will allow apprentices to work with multiple employers in a sector.

– National Minimum Wage

The National Minimum Wage and National Living Wage amounts increase took effect on 1st April 2021. The minimum hourly rate that your staff are entitled to depends on their age and whether they are an apprentice. Follow the link to find out the more.

3 – DLA, Company Cars, Vans and Fuel Benefit

– DLA – Director Loan Rate

If the director’s loan amount exceeds £10,000 at any point during the company’s accounting period, then interest will be charged based on the official rate of interest set by HMRC. As at April 2020 this was 2.25%.

The interest will be charged on the whole amount plus Class 1A National Insurance contributions (13.8%), and may need to be reported on your P11D. If the loan is not repaid within 9 months of the accounting period end, the company pays extra Corporation Tax of 32.5%, repayable by HMRC when the loan is repaid to the company.

– Company cars

The benefit in kind (BIK) tax rates have increased for company cars.

The percentage applied to the list price of the car increases based on the CO2 emissions published by the Vehicle Certification Agency. HMRC has published a ready reckoner you can use to calculate your company car tax.

The tax rate percentage depends on when your car was manufactured, fuel type and CO2 emissions.

The cash equivalent fuel benefit charge has increased to £24,600 (from £24,500) and is calculated by using the same percentage used in the car benefit calculation.

Fully electric cars have no tax charge in the 2020/21 tax year, but there will be a charge on 1% of their list price in the 2021/22 tax year, increasing to 2% in 2022/23.

– Company vans

The BIK fixed amounts for vans have also increased:

- The company van BIK increased to £3,500 (from £3,490)

- The fuel for a van provided for personal use increased to £669 (from £666).

Need help with your P11Ds or perhaps you are considering changing your company car or van and not sure how the new rates will affect the BIK? Contact Onyx now and we will explain how the new rates will affect your end of year tax bill including deductions via payroll.

4 – Student Loans and Postgraduate Loans

– Student Loan Plan 1 and Plan 2 threshold increase

The Department for Education has confirmed that from 6th April 2021 the earnings threshold before you start to repay a Student Loan for:

- Plan 1 loans has risen to £19,895 (from £19,390)

- Plan 2 loans has risen to £27,295 (from £26,575)

- A new Plan 4 scheme is being introduced for all new and existing Scottish loans with a threshold of £25,000 – anyone with an existing Scottish loan will be moved from their existing Plan 1 to Plan 4.

If you are a director being paid salary and dividends from your company, and you are paying back a student loan, you must remember the threshold for repayment is based on your total income.

– Postgraduate Master’s Loan and Postgraduate Doctoral Loan

This was first introduced in the 2020/21 tax year. A Postgraduate Master’s Loan is a new type of loan introduced by the government to help with course fees and living costs while studying a postgraduate master’s course. The repayment of a Postgraduate Loan is treated the same as any other Student Loan and interest is charged from the day the first payment is received.

Repayment is calculated at 6% for students in England and Wales on income above £21,000. The rate is 9% for Scottish and Northern Ireland students with income above £18,330.

5 – Other personal tax reliefs and allowances

– Personal pensions

The tax-free amount you can pay into a Personal Pension remains unchanged at £40,000 for the 2021/22 tax year. The lifetime allowance for pension savings also remains unchanged at £1,073,100 and will be frozen until 2026.

– Inheritance Tax

There is no change to the Inheritance Tax (IHT) nil rate band, the threshold remains at £325,000 and is frozen at that level until 2026.

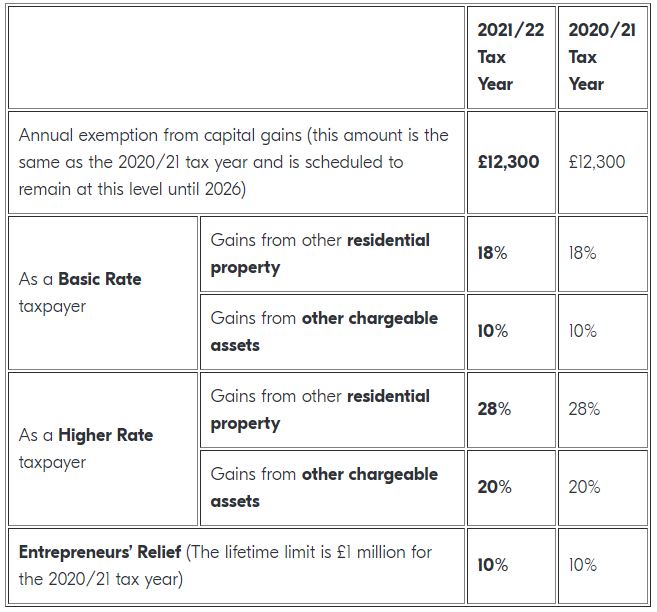

– Capital Gains Tax

The Capital Gains Tax annual exempt amount for individuals remains unchanged at £12,300 for the 2021/22 tax year and will be frozen at that level until 2025/26.

There have been no changes to the capital gains tax rates for gains taxable in both the basic rate and higher rate tax bands. The period allowed to pay any CGT on property sales to HMRC will be reduced to 30 days from the date of sale. These changes took effect from 6th April 2020.

6 – Entrepreneurs’ Relief

From 6th April 2020 the Entrepreneurs Relief lifetime allowance limit was capped at £1 million. This is a significant reduction from the £10 million limit that was in existence in the 2019/20 tax year.

The capital gains tax rate remains unchanged at 10%.

Thinking about selling an investment property, other capital investments or perhaps you are considering a capital investment purchase? Contact Onyx now and we will discuss the options available to maximise on capital profits, utilise those potential losses and how to budget for the capital gains tax bill so there are no nasty surprises.

7 – VAT, Corporation Tax, workplace pensions and allowances

– VAT

Registration Threshold – The level of revenue at which you must register for VAT remains unchanged at £85,000.

Deregistration Threshold – The level of revenue at which you may consider to deregister for VAT remains unchanged at £83,000.

Standard rate of VAT remains at 20% and the Reduced rate of VAT remains at 5%.

In the March 2021 Budget, the Chancellor said that both VAT thresholds would be maintained until 31st March 2024.

– Temporary reduction in VAT for the hospitality and tourism sector

In July 2020, as part of the government’s economic measures to respond to the COVID-19 emergency, VAT in the hospitality and tourism sector was reduced from 20% to 5%. In the March 2021 Budget this was extended to 30th September 2021, and it was also announced that an intermediate rate of 12.5% would apply for qualifying supplies from 1st October 2021 to 31st March 2022, after which it would return to the Standard Rate of 20%. The sector includes food outlets, providers of accommodation such as hotels and guest houses, and attractions such as cinemas and theme parks.

– Corporation Tax

Corporation Tax payable on business profits remains unchanged at 19%. However, in the March 2021 Budget, the Chancellor announced plans for increases to Corporation Tax from 2023. It will increase to a rate of 25% for businesses with profits above £250,000. Then a reintroduction of the ‘Small Profits Rate’ of 19% for businesses with profits below £50,000. Between £50,000 and £250,000, there will be a tapering calculation, further details will be announced in due course.

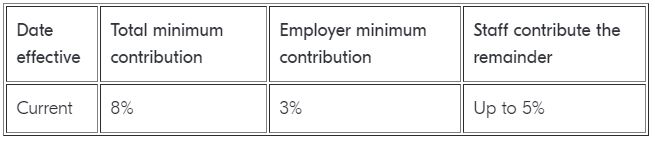

– Workplace pensions (auto-enrolment)

There are no changes to the minimum amount you need to pay into your employee’s auto-enrolment workplace pension. This means the total amount of employer and employee contributions remains a minimum of 8% of your employee’s qualifying earnings.

– Annual Investment Allowance (AIA)

Companies will be able to claim £1 million as AIA for expenditure incurred between 1st January 2019 and 31st December 2021 on fixed assets such as plant and machinery. No further changes have been announced however it is anticipated that there will be a reduction in 2022.

– Business Investment Tax Relief and Loss Relief for Business

A new “super-deduction” tax relief was announced for businesses to reduce their tax bill by 130% of what they spend on investment. The Chancellor also announced the extension of the normal loss carry-back rules from one year to three years for losses of up to £2 million. This will enable tax repayments to be claimed, providing relief and cash flow support for businesses.

– Business rates

The government had intended to carry out a review of Business Rates, however this has not happened due to Covid-19.

From 1st April 2021, eligible businesses in the retail, leisure and hospitality sectors will continue to benefit for a 100% business rates relief until 30th June 2021. This includes hotels, restaurants and coffee bars.

This will be followed by 66% business rates relief for the period from 1st July 2021 to 31st March 2022, capped at £2 million per business for properties that were required to be closed on 5th January 2021, or £105,000 per business for other eligible properties.

Nurseries will also qualify for relief in the same way as other eligible properties.

8 – Other Taxes and COVID-19 Support

– SEISS

In the March 2021 Budget, the chancellor announced further support for the self-employed to include a fourth and a fifth round of income support grants.

The fourth SEISS grant is available to individuals who began self-employment in the 2019/20 tax year, which began on 6th April 2019, as well as those who have previously claimed.

Individuals who are eligible will be able to claim the fourth round of SEISS at 80% of average trading profits capped at £7,500 for three months. The fourth grant will be available later this month.

The fifth and final grant will cover May, to September, and should be available in late July. The amount you receive will depend on how badly your business has been affected.

If your self-employed business turnover has fallen by 30% or more, you’ll receive 80% of 3 months’ average trading profits, capped at £7,500. Or for those with a turnover reduction of less than 30%, you’ll receive 30% of 3 months’ average trading profits, capped at £2,850.

To be eligible for the fourth grant, and for new entrants to the scheme, you must have filed a Self Assessment tax return for the 2019/20 tax year by midnight on 2nd March 2021. All other eligibility criteria will remain the same as the third grant.

HMRC have provided an online tool to check if you’re eligible. If your business continues to be affected and you received the first three grants then you are likely to be eligible for the additional grants. The government has an online portal for making a claim which will open shortly when the fourth grant is available.

– CJRS Furlough Scheme

In the March 2021 Budget, the Chancellor announced the extension of the furlough scheme (Coronavirus Job Retention Scheme or ‘CJRS’) until the end of September 2021. Workers will continue to receive 80% of their current salary for hours they do not work due to furlough.

Employers will need to make a contribution of 10% of the worker’s salary for unworked hours in July 2021, and a 20% contribution in August and September 2021. The £2,500 monthly limit for the grant remains in place.

The planned introduction of the Job Support Scheme has been postponed until the CJRS scheme has ended. This also applies to the Job Retention Bonus which has been temporarily withdrawn.

The Job Support Scheme will not be a direct replacement for the CJRS. Employers will continue to pay an employee for time worked, but the costs of hours not worked will be split between the employer and the government (through wage support) and the employee (through a wage reduction). Importantly, the employee will keep their job.

The government had previously announced that there would be a £1,000 Job Retention Bonus available to employers in February 2021. However, due to the extension of the CJRS scheme, this has now been suspended. The government has said they will not pay the Job Retention Bonus in February 2021. Instead it will redeploy a retention incentive at the right time.

The original plan was that employers would be able to claim a one-off payment of £1,000 for every employee they have previously received a grant for under the Coronavirus Job Retention Scheme (CJRS) and who remains continuously employed until 31st January 2021. HMRC will release further guidance on this bonus in due course.

– Business Recovery Loan Scheme

From 6th April 2021, the Recovery Loan Scheme will provide lenders with a guarantee of 80% on eligible loans between £25,000 and £10 million. The scheme will be open to all businesses. This includes those who have already received support under the existing COVID-19 guaranteed loan schemes.

– Grants Schemes

New ‘Restart Grants’ to help businesses in England reopen when lockdown begins to ease from April 2021 are:

- Non-essential retail businesses will receive grants up to £6,000 per premises.

- Hospitality and leisure, including personal care and gyms, which are more impacted by restrictions and may not open until later in the year, can each receive grants of up to £18,000.

Information on additional local authority grants are available from your local council.

– Alcohol and Fuel Tax

Alcohol and fuel duty remains frozen for the next 12 months and the planned increases have been cancelled.

– Stamp Duty Land Tax

The stamp duty holiday for the first £500,000 Nil Rate Band of the purchase price will continue until the end of June 2021. From 1st July 2021, the Nil Rate Band will reduce to £250,000 until 30th September 2021 before returning to £125,000 on 1st October 2021.

– Mortgage Guarantee Scheme

A new mortgage guarantee scheme starts in April 2021. This scheme will provide a guarantee to lenders across the UK who offer mortgages to people with a deposit of just 5% on homes with a value of up to £600,000. All buyers will have the opportunity to fix their initial mortgage rate for at least five years.

The scheme will be available for new mortgages up to 31st December 2022. It will increase the availability of mortgages on new or existing properties for those with small deposits.

You can read further guidance in our Budget 2021 Report and also the latest COVID-19 news to ensure you are receiving the right financial support.

Worried about how your business may be affected during the months ahead? Contact Onyx now.

Need help? Get in touch with Onyx

If you need help, or want to discuss further, please give us a call us or e-mail us at enquiries@onyx.accountants for a FREE no obligation consultation.

Got any questions or queries? Our friendly team are happy to help. Just drop us a line! Call us on 0121 753 5522 or 01902 759 800.

")